- Get started on your mortgage

- Buying your first home, next home, investing in property or just keen to review your mortgage?

- Apply online

- Put your savings to work

- Earn better returns and access your money with no penalties.

- Start investing now

Rodney's Ravings: The case for a market-led fall in interest rates

Guest post from Rodney Dickens

In an ideal world, the Reserve Bank (RB) would make quality decisions about the official cash rate (OCR) that would contribute to a more stable economic environment than would otherwise be the case.

Instead, the RB regularly makes bad decisions, is slow to realise when it is wrong and is a major source of instability in the economy that particularly impacts on the housing market.

Governor Orr has been effectively forced to acknowledge he over-stimulated the economy in response to Covid, and the RB is now scrambling to make up for that mistake by hiking the OCR aggressively. However, in the process it is making another mistake.

As discussed in my article last month, the RB has a multi-year inflation battle on its hands because it overstimulated the economy. This is something that’s best measured by the unemployment rate being allowed to fall well below the level consistent with the RB’s consumer price index inflation target.

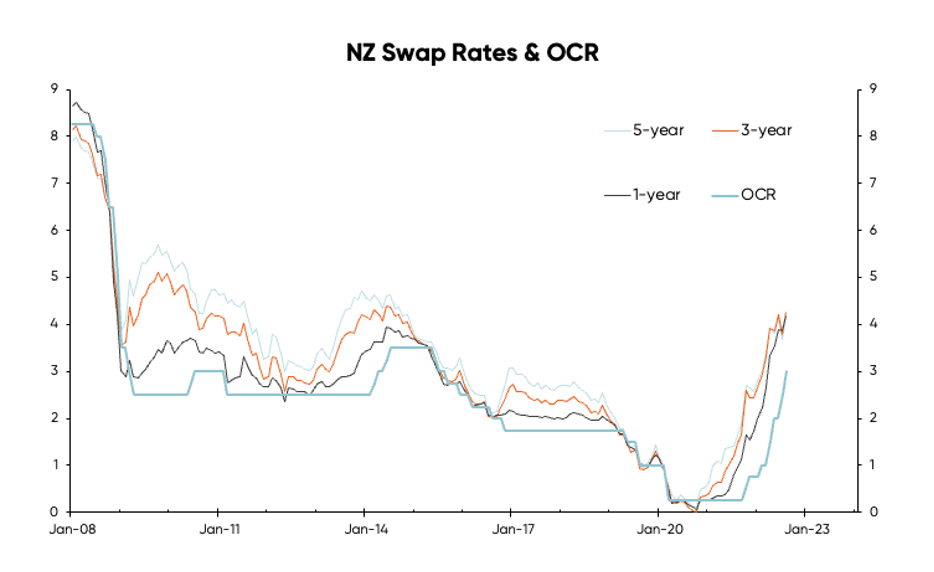

In response, the RB has hiked the OCR from 0.25% in October 2021 to 3% now and plans more hikes.

As a result, the average mortgage rate offered by the major banks has increased from a low of 3.2% to 5.7% currently. This represents a 78% increase in interest costs, well over the 53% increase over the whole period the RB last battled inflation, between 2004 and 2008. If the RB keeps hiking as planned, there could be up to a 100% increase in mortgage interest costs.

It should be no surprise that consumer and business confidence surveys have tumbled into recessionary territory, retail spending has fallen in the last two quarters, the housing market has been trashed and leading indicators point to around a 40% fall in residential building activity.

Despite the sharpest increase in interest rates ever, leading indicators pointing to an imminent recession, and anecdotes from the building industry saying a major fall in activity is coming, the RB is still predicting moderate economic growth over the next year and only a modest 6% fall in residential building activity over the next two years.

In its rush to make up for the mistake of overstimulating the economy in response to Covid, the RB is now moving ahead blindly with OCR hikes without properly assessing the impact of the hikes so far.

It will no doubt continue to hike more this year, despite clear signs it has already done enough damage to justify pausing to give time to properly assess the impact.

The excess stimulus the RB delivered in response to Covid and the blind rush to keep hiking now reflect poor judgement by the RB, and it being out of touch with what is going on in the economy.

By contrast, the market, while not being able to see into the future, is much quicker to respond to news about the economy than the RB.

Before the latest OCR hike and hawkish rhetoric by the RB, the market was starting to nudge down wholesale or swap rates as shown in the chart above. Swap rates regularly move up and down ahead of the OCR because the market is quicker than the RB to respond to economic news.

The current five-year swap rate, for example, reflects what the market expects the OCR to be over the next five years so is freer than the one-year rate to deviate from the current OCR. But even the one-year rate regularly moves up and down ahead of the OCR.

The market doesn’t always get it right. However, if economic growth and residential building activity turn out much worse than the RB and market currently expect, as seems likely, a market-led fall in interest rates should occur even if the RB remains slow to realise the extent of damage being done by the sharpest increase in interest rates ever.

By Rodney Dickens, Managing Director, Strategic Risk Analysis Ltd www.sra.co.nz.

Enjoying our blog? Get the latest sent straight to your inbox

Receive updates on the housing market, interest rates and the economy. No spam, we promise.

The opinions expressed in this article should not be taken as financial advice, or a recommendation of any financial product. Squirrel shall not be liable or responsible for any information, omissions, or errors present. Any commentary provided are the personal views of the author and are not necessarily representative of the views and opinions of Squirrel. We recommend seeking professional investment and/or mortgage advice before taking any action.

To view our disclosure statements and other legal information, please visit our Legal Agreements page here.