- Get started on your mortgage

- Buying your first home, next home, investing in property or just keen to review your mortgage?

- Apply online

- Put your savings to work

- Earn better returns and access your money with no penalties.

- Start investing now

Rodney's Ravings: Economists are a threat to your financial wellbeing

Guest post by Rodney Dickens

Mortgage borrowers have been burnt badly by massive increases in interest costs since mid-2021.

When the increases started, roughly 80% of all bank mortgages were either on floating rates (13%) or fixed for a year or less (66%). Those numbers are well above normal levels, which hover around 60-65%, and meant borrowers were especially vulnerable to the massive increase in interest rates.

Some of the blame for this lies with economic forecasters

In mid-2021, more borrowers than normal were taking a punt that interest rates wouldn’t increase enough to warrant fixing for more than a year. At the time, the average one-year fixed rate among the major banks was 2.2%, the average three-year rate was 3% and the average five-year rate was 3.9%.

So, if interest rates weren’t really going anywhere, of course it made sense to fix short-term, rather than opt into the higher rates that came with fixing for more than a year.

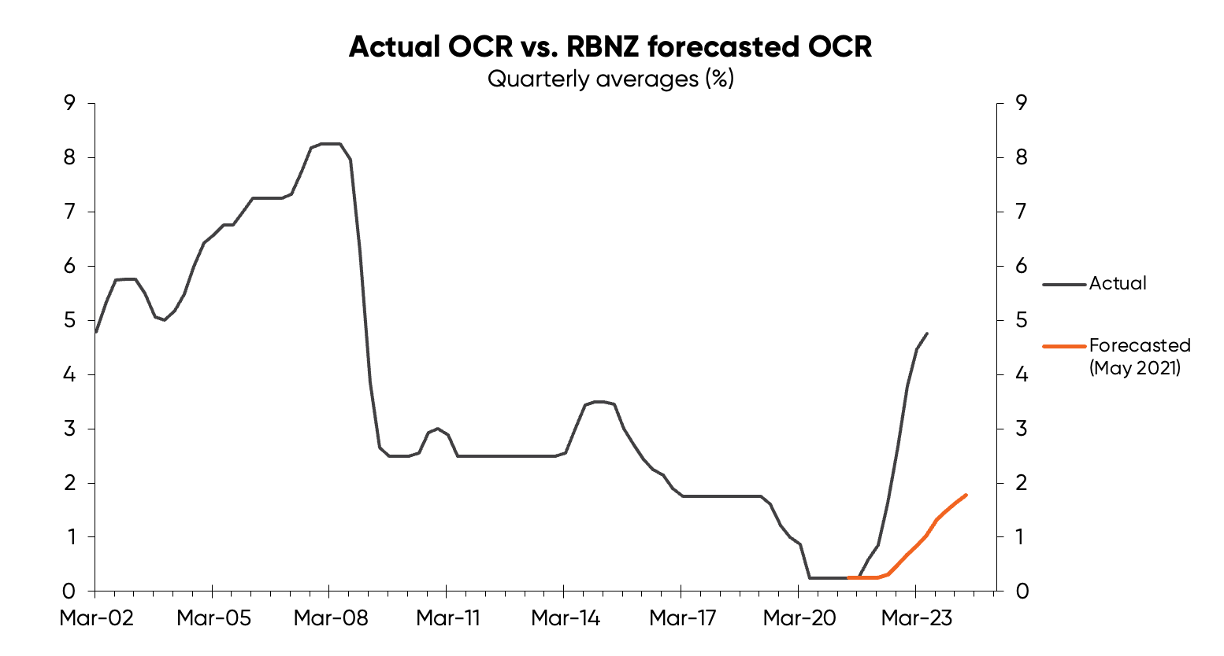

In May 2021, the Reserve Bank (RBNZ) predicted it would take three years for the OCR to return to its pre-Covid level of 1.75%. The orange line in the chart below tracks the RBNZ's predictions, against what's actually eventuated.

This forecast was a by-product of the RBNZ prediction that CPI inflation would slowly increase to 2% (the mid-point of its target) by September 2023. And the bank economists were generally forecasting less upside in the OCR than the RBNZ.

In reality, by June 2022 inflation had surged to a peak of 7.3%, and the OCR has just gone up another 0.50% to 5.25% – and borrowers have been burnt more than needed to be the case because few had fixed for more than a year.

Predictions from economic forecasters that interest rates would only rise slowly, and that they wouldn’t hit pre-Covid levels, have played a part in borrowers being poorly equipped to weather the massive increase in interest costs.

Hindsight’s a beautiful thing – and it’s easy to see now what borrowers should have done

But the fact is that well before mid-2021 there were warning bells about the inflation threat. Warning bells which economic forecasters ignored. Even without the benefit of hindsight, they should have been well aware that fixing short-term in mid-2021 was a risky move.

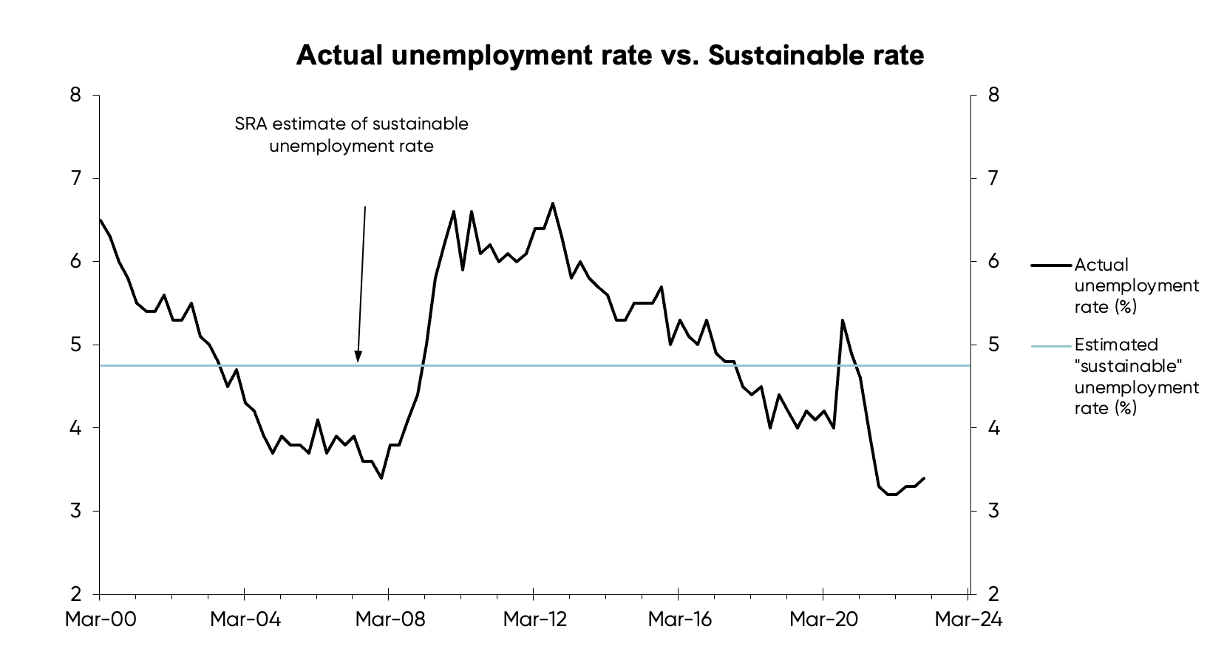

This next chart, below, is one of my favourites. It shows the unemployment rate and my estimate of the sustainable unemployment rate, consistent with the RBNZ’s inflation target (the blue line). The current 3.4% unemployment rate is a testimony to the RBNZ having hugely overstimulated the economy, giving too much bargaining power to employees and setting off a wage-price spiral.

Covid supply disruptions and global energy market developments, only partly related to Russia’s invasion of Ukraine, significantly added to inflation – but there was solid cause for concern about inflation well before the pandemic, which should have escalated after Covid.

That was thanks to excessive stimulus from the RBNZ, resulting in the unemployment rate falling well below the level consistent with its inflation target.

An inflation problem was in the pipeline well before mid-2021, even though the bank economists didn’t see it coming.

And that's why taking notice of what they forecast can be a threat to your financial well-being.

Enjoying our blog? Get the latest sent straight to your inbox

Receive updates on the housing market, interest rates and the economy. No spam, we promise.

The opinions expressed in this article should not be taken as financial advice, or a recommendation of any financial product. Squirrel shall not be liable or responsible for any information, omissions, or errors present. Any commentary provided are the personal views of the author and are not necessarily representative of the views and opinions of Squirrel. We recommend seeking professional investment and/or mortgage advice before taking any action.

To view our disclosure statements and other legal information, please visit our Legal Agreements page here.