- Get started on your mortgage

- Buying your first home, next home, investing in property or just keen to review your mortgage?

- Apply online

- Put your savings to work

- Earn better returns and access your money with no penalties.

- Start investing now

The RBNZ signalled we were done – so why are mortgage rates still going up?

Post by David Cunningham - Chief Squirrel

NB: Rates accurate as at 28th July 2023.

Right now, mortgage interest rates are doing something they shouldn’t be.

Over the last month or so, all of our main banks have moved to hike their fixed mortgage rates by about 0.25%. For a homeowner with a $500,000 mortgage, that difference is going to cost them about $100 more every month in mortgage interest payments.

Why that’s weird, is because it’s happening despite the Reserve Bank signalling – not once, but twice – that we’re likely at the peak of the interest rate cycle.

A reminder of the Reserve Bank’s stance on interest rates:

During its two most recent Official Cash Rate (OCR) reviews, on 24th May and 12th July, the RBNZ has said it’s expecting rates to stay “at a restrictive level for the foreseeable future” as we try to get inflation back within the 1% to 3% target range. The timeframe they’ve given us is mid-2024.

The implication is that we shouldn’t need any further OCR hikes to get us there, and so the OCR should stick at 5.50% in the meantime.

And yet, banks have continued to hike interest rates for borrowers. Why?

By increasing fixed mortgage rates as they have, banks have effectively delivered a similar outcome to another quarter-percent hike in the OCR.

The move has been driven by two factors.

Firstly, wholesale interest rates (which set the benchmark for bank mortgage rates) for 2- to 5-year terms have risen by about 0.25% since the 24th May OCR review. You can see this shift in the bottom three lines on the below graph:

![]()

Data source: interest.co.nz

Incidentally, longer-term rates are sitting lower than the shorter-term rates, as a reflection of the fact that markets are expecting the OCR to start falling in 2024.

Secondly, although 1-year wholesale interest rates have barely moved, banks have expanded their margin on 1-year home loan rates by about 0.25%. At present, this is the most popular term for home loan borrowers, keen not to be locked in once rates do start to fall.

![]()

Data source: interest.co.nz (average bank 1-year fixed interest rate, wholesale swap rates)

It’s important to acknowledge that banks have also increased term deposit interest rates, particularly for six and 12-month terms, by about 0.25%. Term deposits make up a sizeable portion of bank funding, so the interest rate moves, in tandem, are probably neutral for overall bank margins.

In essence, these hikes achieve one thing and one thing only: protecting record-high bank margins

Bank margins are already at elevated levels, as shown in the graph below.

![]()

Source: RBNZ Bank Dashboard, average of the five major banks. June margin is an estimate.

I’ve written previously about the main reason for this margin growth – which is that the banks haven’t passed on interest rate increases to savings account holders at the same pace the OCR has climbed. In other words, Kiwi with money sitting in bank savings accounts (to the tune of about $75 billion) are supporting about $1.5 billion p.a. of higher bank pre-tax profits.

|

|

Official Cash Rate |

Bank Savings Accounts Average Interest Rate |

Difference |

|

June 2018 |

1.75% |

1.19% |

0.6% |

|

June 2019 |

1.50% |

1.02% |

0.5% |

|

June 2020 |

0.25% |

0.33% |

-0.1% |

|

June 2021 |

0.25% |

0.15% |

0.1% |

|

June 2022 |

2.00% |

0.82% |

1.2% |

|

June 2023 |

5.50% |

3.5% |

2.0% |

Data source: Reserve Bank. June 2023 bank savings rate is an estimate based on May 2023 data.

And by choosing to hike fixed home loan interest rates as they have, the banks are protecting these margins – the highest we’ve seen in at least five years – and in turn helping to drive record bank profits.

So…where to from here?

The latest Consumer Price Index stats show inflation has fallen to 6.0%, slightly below what the RBNZ had forecasted. And while it’s a good sign that we’re starting to get inflation under control –non-tradable (or domestic) inflation is still proving sticky.

The result has prompted some economists to predict another 0.25% lift in the OCR, with wholesale markets pricing a 60% chance of another 0.25% hike by November 2023.

So, despite the Reserve Bank’s pretty clear stance on the issue, the jury (a.k.a. “the market”) is still out on whether there’ll be another hike in the OCR.

My opinion is that the Reserve Bank will stick to its guns and hold the OCR at 5.5% until early 2024.

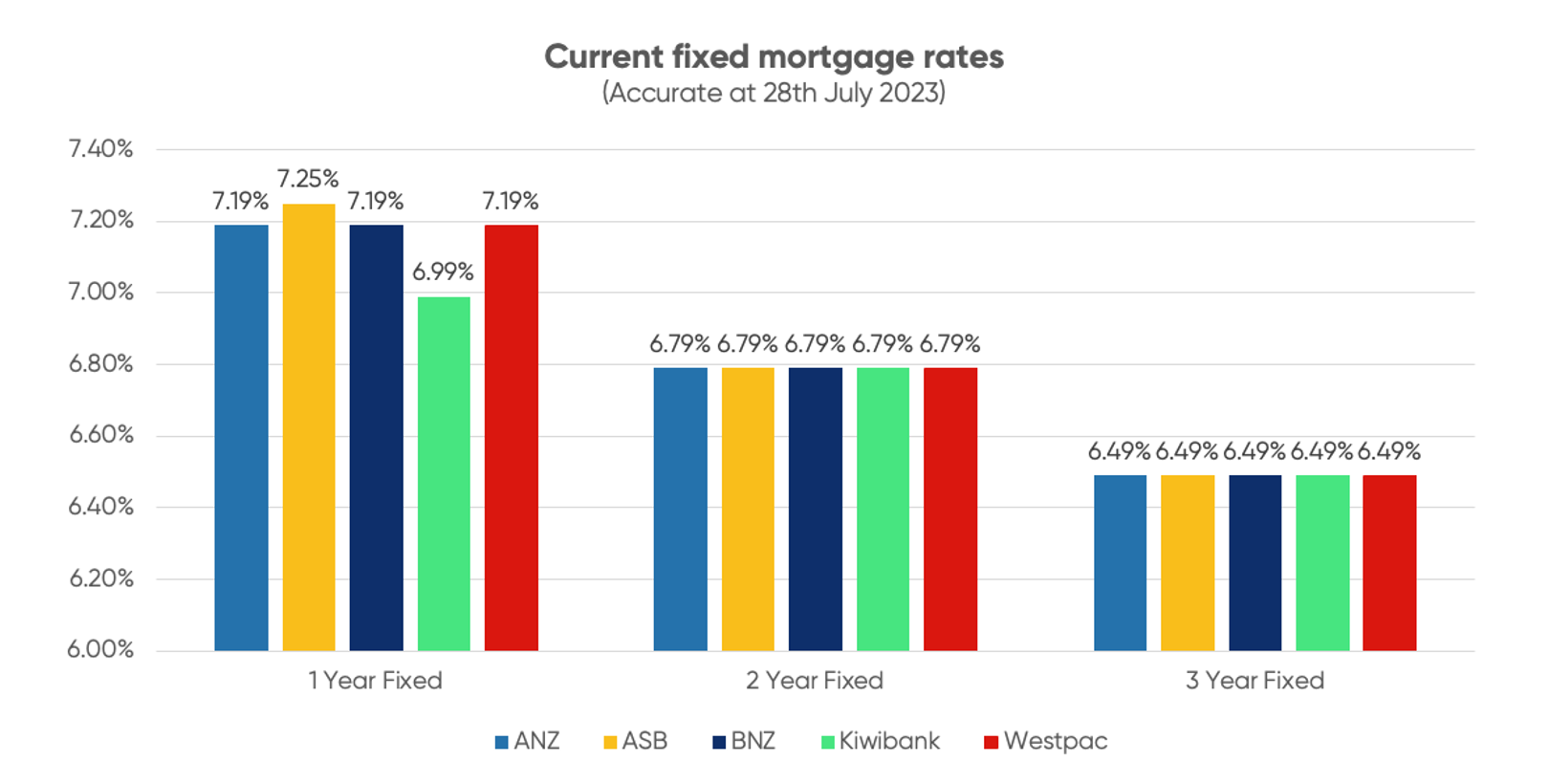

And on the home-loan front… the below chart tracks current fixed mortgage rates across our five major banks:

Data source: interest.co.nz

Given the way banks operate – always moving in tandem – it’s unlikely we’ll see any significant reduction in fixed home loan rates until wholesale interest rates fall and force the banks’ hand. We know they won’t deliberately get themselves into an interest rate war.

But, as we start to see more evidence of lower inflation, continuing weak economic growth, and higher unemployment, my view is that the market will slowly start to price in falls in the OCR. That could see wholesale markets swap rates, and therefore home loan interest rates, fall sharply.

The unfortunate news for home loan borrowers is that could still be several months away.

The opinions expressed in this article should not be taken as financial advice, or a recommendation of any financial product. Squirrel shall not be liable or responsible for any information, omissions, or errors present. Any commentary provided are the personal views of the author and are not necessarily representative of the views and opinions of Squirrel. We recommend seeking professional investment and/or mortgage advice before taking any action.

To view our disclosure statements and other legal information, please visit our Legal Agreements page here.