New Zealand house prices have been on a wild ride in recent years.

Partly, this was down to the Reserve Bank’s response to the pandemic—but adding to this was the collective Covid “mania” that drove prices up much more than justified by the normal demand-supply measures, followed by Covid regret that reversed this excessive price increase.

Four years on, house prices are now behaving roughly as expected, based on the demand-supply balance that implies more near-term downside

Earlier predictions from bank economists were that we would see solidly rising prices this year, but those predictions were out of touch with where we’re at in the economic cycle, which plays a significant part in house price cycles. Prospects will improve soon driven by falling interest rates, but it is still too early to expect significant upside in house prices.

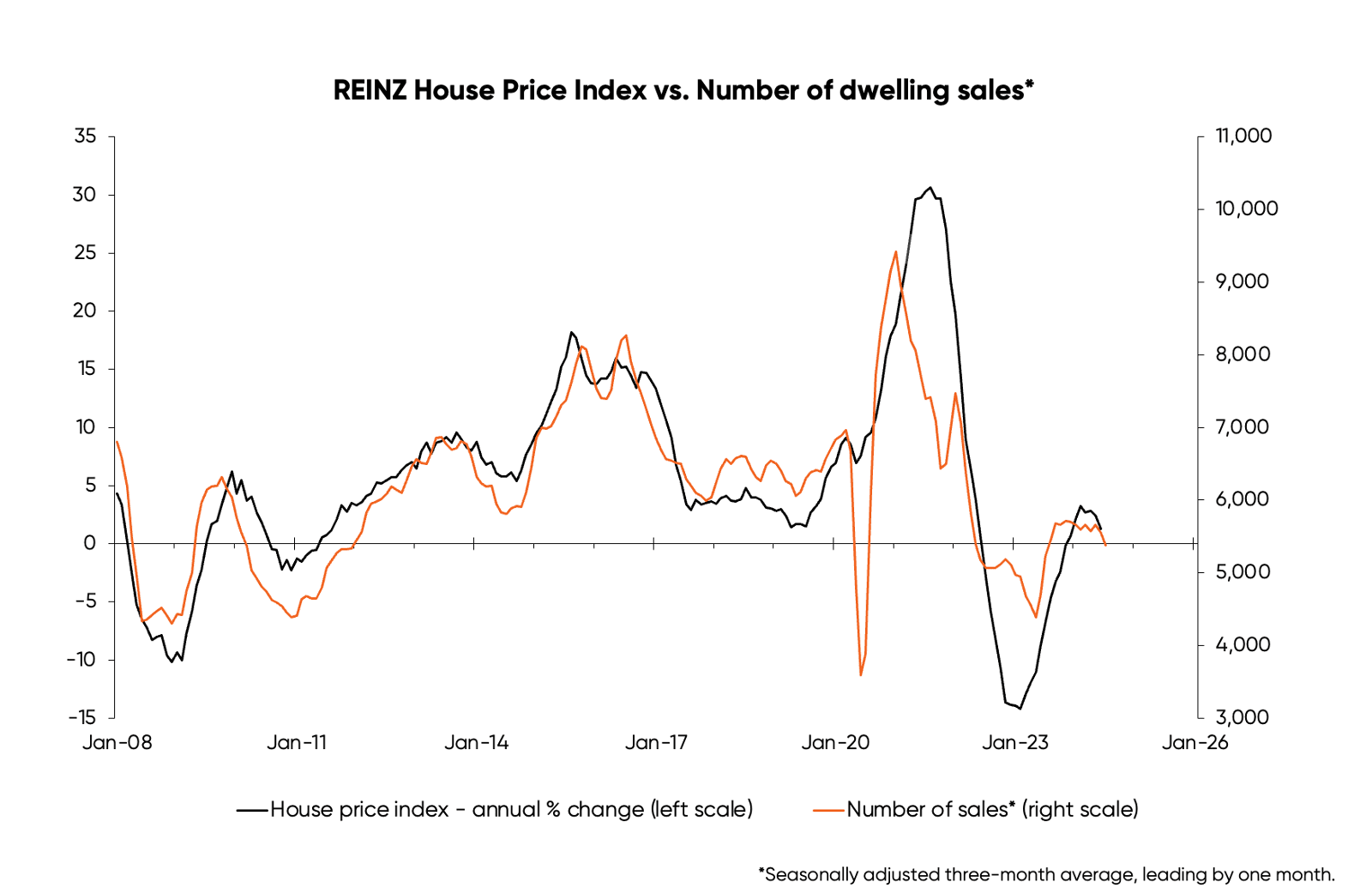

After our first lockdown ended, in 2020, house prices surged at their fastest pace ever—up 44% between May 2020 to November 2021, according to the REINZ NZ House Price Index (first chart, below)—taking them well above the trend line. This was followed by the sharpest ever recorded fall—as prices dropped 17% between November 2021 and April 2023—taking them back below the trendline, as is quite normal in recessions.

Although the Reserve Bank’s (RBNZ) actions—slashing interest rates and temporarily removing LVRs—certainly helped to drive a surge in sales after the lockdown-driven tumble in late-March and 2020 (red line, second chart), there was more to it than that.

In 2021, prices surged well above the level predicted by the number of sales, as shown by the gap between the two lines in the chart.

This was the result of Covid mania: where, after having spent lots of time at home during lockdown, people scrambled to upgrade and many were willing to overpay in order to do so—aided by low interest rates and the lack of LVRs.

Then, a market-led increase in interest rates (starting in April 2021) coupled with the reintroduction of LVRs in March 2021, drove dwelling sales below pre-Covid levels in 2022/23 (second chart, below).

This time house prices fell far further than expected, based on the fall in sales in 2022/23, as Covid “mania” was replaced by Covid “regret”—and the artificially high level of prices was unwound.

The REINZ NZ House Price Index did not fall back to the pre-Covid level, but it did fall far enough to be roughly back in line with the rising trendline, after allowing for the tough economic times justifying prices falling slightly below the trend line (top chart).

But now, the Covid joyride appears to be over

The annual percent change in the REINZ House Price Index is back to being roughly in line with where it should be, given the level of sales (as per the second chart).

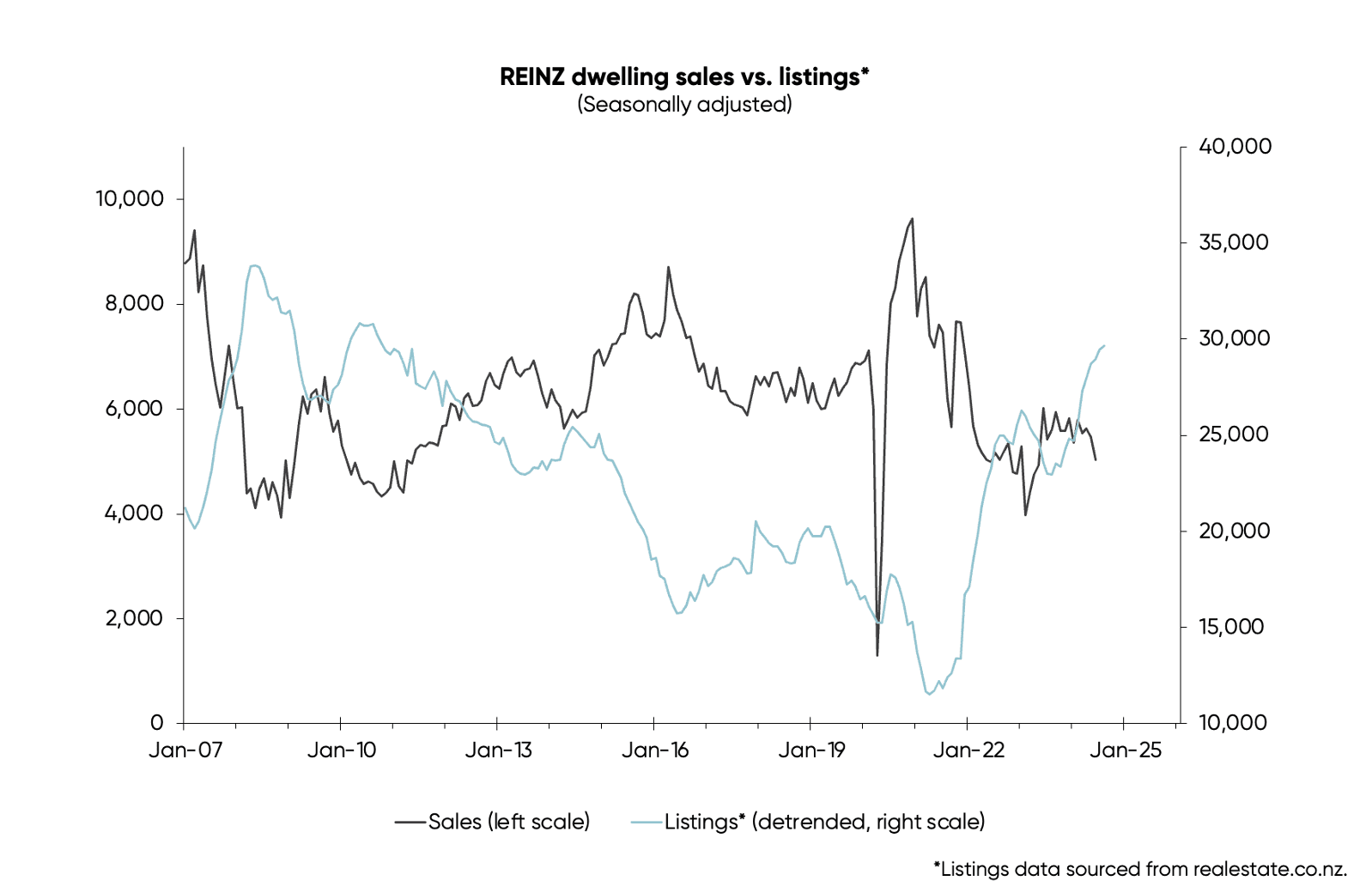

The recent fall we’ve seen in prices—which is likely to continue a bit longer—is to be expected given the demand-supply balance as measured by REINZ sales vs. listings on www.realestate.co.nz (shown in the third chart), with listing numbers higher than sales indicating downside for prices.

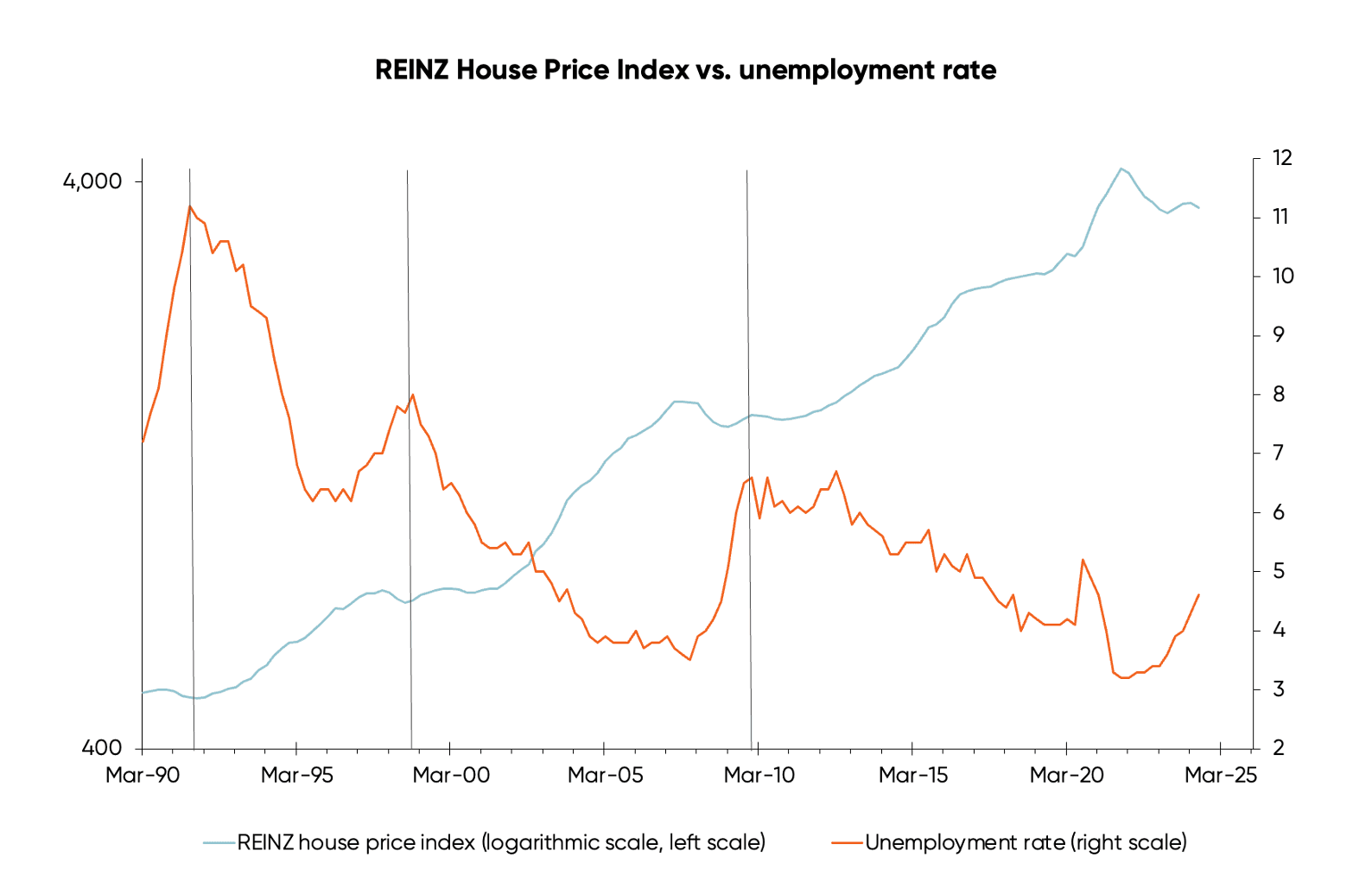

After getting ahead of themselves in predicting a house price recovery, some of the bank economists have been scaling down expectations. It’s normal for major increases in prices not to start until after the unemployment rate has peaked (fourth chart).

The vertical lines identify previous peaks in the unemployment rate—excluding the Covid peak in 2020, which was an anomaly. House prices typically bottom out near peaks unemployment rate, while significant upside doesn’t occur until sometime after that peaks.

Interest rates may have already fallen enough to mean house price will level out later this year, but will have to fall quite a bit further before house prices start to rise significantly.

By Rodney Dickens, Managing Director, Strategic Risk Analysis Ltd www.sra.co.nz.