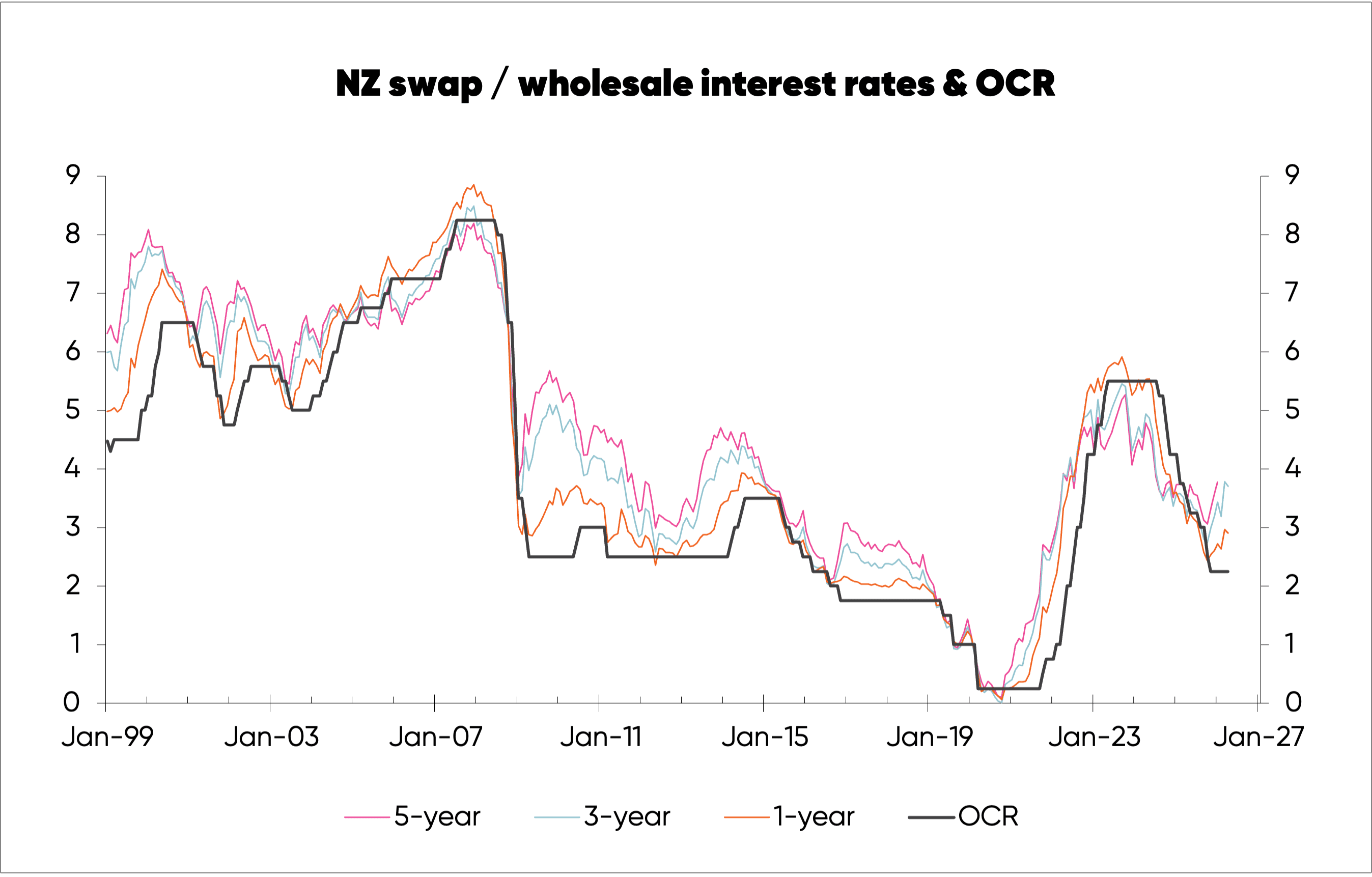

It is quite normal for the market to push up swap or wholesale interest rates ahead of OCR hikes as it was doing even before the US-Israel war on Iran (first chart).

The market prices in new information quickly—whereas, because the Reserve Bank (RBNZ) only reviews the OCR seven times a year (outside of emergencies), it can be slow to react to new information.

There have been times when the market has got it wrong, though, such as when it pushed up swap rates in 2009.

Yes, the RBNZ subsequently delivered two 0.25% OCR hikes in mid-2010, but they didn’t last long and were less than the market had expected. The rise in inflation the market had anticipated when it began pushing up swap rates never arrived, and over time swap rates fell back towards the OCR.

Prior to the war on Iran, I saw good reason for the market to start nudging up interest rates.

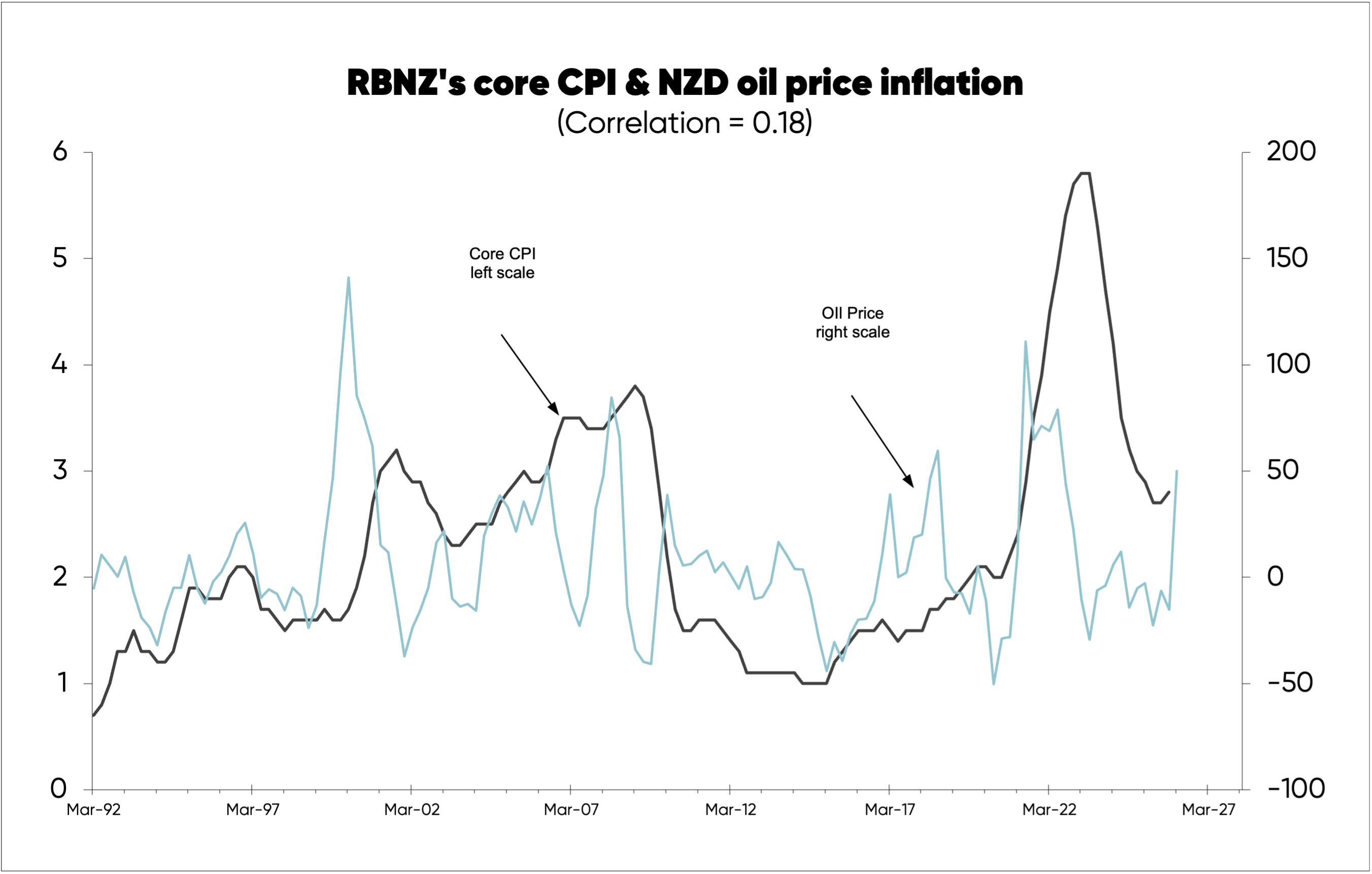

The tail-end of the OCR cuts in 2025 were based on too-negative expectations about our recovery from the 2024 recession. Meanwhile, the RBNZ’s measure of core CPI inflation, which excludes volatile items like energy prices, nudged up to 3.1% in Q4 2025 (shown as the grey line in the second chart).

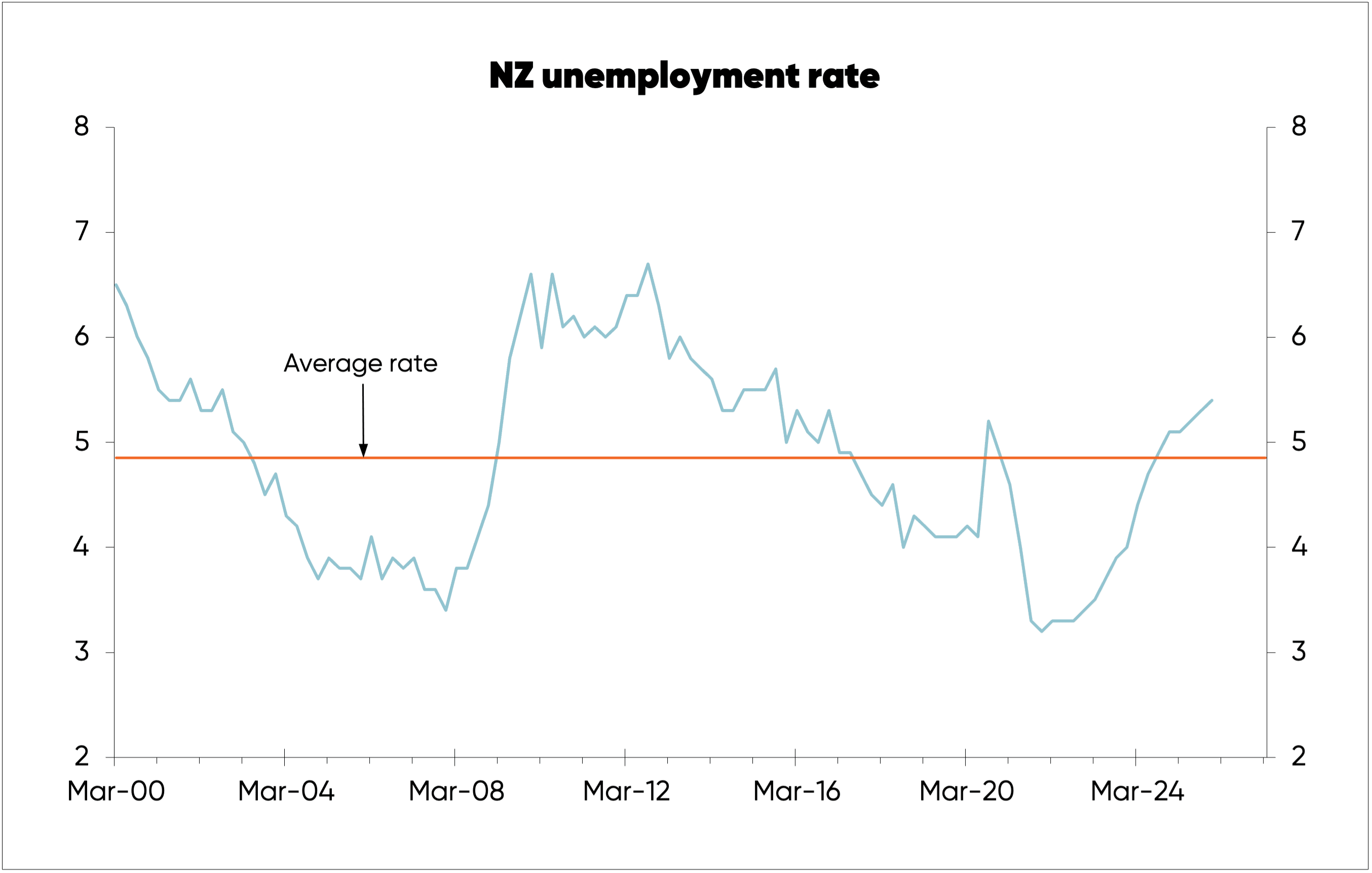

On the flip side, supporting the RBNZ’s intention to not start hiking the OCR until the end of the year (as outlined in its February forecasts), there is some spare capacity hanging around in the economy, with the unemployment rate currently sitting above average (third chart).

Business and consumer confidence surveys have started to fall in response to the war and may fall enough to mean spare capacity will help keep core CPI inflation under control for some time.

Also working in the RBNZ’s favour is the fact that, historically, there hasn’t been much of a link between oil price inflation and core CPI inflation (refer to the second chart, above).

My sense is that the market, and NZ swap rates, may be responding too sharply to the highly visible inflationary impact of the war—spiking petrol and diesel prices at the pump—without considering the negative impact the war will have on economic growth, that is yet to show up in the official economic data.

It’s a hard thing to assess because there are no useful precedents.

The oil price shocks in the 1970s aren’t good precedents in my assessment because they were in part responses to a major global inflation problem that existed before the first oil price shock in 1973.

Reality may lie somewhere between the RBNZ’s head-in-the-sand view and the market’s view, which may be focused too much on the inflationary implications of the war versus the negative impact it will have on economic growth.

These are uncertain times and it is hard to assess which view is correct. My best guess is the market is getting a bit ahead of itself in worrying about medium-term inflation prospects.

About the author: Rodney Dickens, Strategic Risk Analysis - Managing Director

As far as economists are concerned, Rodney’s about as seasoned as they come. Having started out his career at the RBNZ—including a stint on its Monetary Policy Committee—he’s held roles as Head of Research and Chief Economist inside several of New Zealand's big banks and leading financial institutions, and worked for the Bank of England. He launched Strategic Risk Analysis in 2006, regularly reporting on the state of the economy, housing market and interest rates.