Let’s kick this month’s investor update off with a little look at what's been happening on the platform itself, because that’s where your money’s working hard every day.

Platform update

For anyone who missed the news, thousands of Kiwi have now invested over $500 million with Squirrel.

Our investor community has also grown to more than 12,000 active investors—a huge milestone, and it’s all thanks to you.

Behind the scenes, things are ticking over nicely:

- Loan portfolio: remains in good health, with our credit team keeping borrowers on track

- Reserve funds: continuing to build, giving you that extra layer of protection

- Wait times to invest: have been jumping around a bit more recently, but we’ve seen a better balance over the past month. Right now, wait times have increased slightly, but a heap of new loans are expected to settle over the next 2 – 3 weeks.

We’ve had a few questions come in about how the Monthly Income Fund works – so we’ve written a blog that explains it all, from how returns build and reset each month to your payout options.

Interest rates: lower for longer?

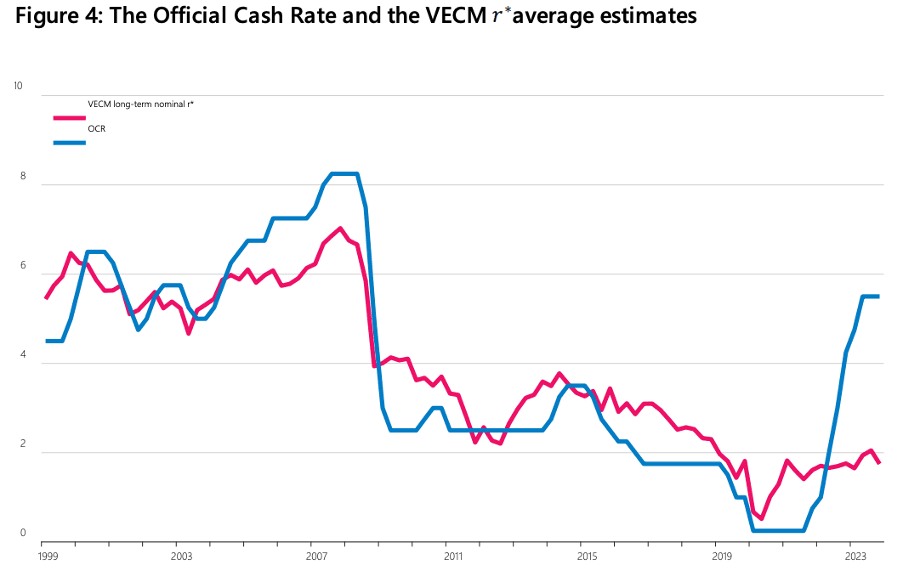

Earlier this month the RBNZ published a research note estimating where the ‘neutral’ OCR might sit. That’s basically the sweet spot where rates are neither heating up nor cooling down the economy.

The chart below (pulled from that note) shows just how hard they “uppercut” the economy to get inflation under control.

And while inflation’s still hanging around the top of the target band, the RBNZ’s challenge is how far and how fast they ease back to create stable inflation in the 1%-3% target range. The pink line shows the calculated neutral OCR, and the blue line is the actual OCR.

Our take? If you look back over the past four years, Squirrel called early that rates needed to rise before the RBNZ finally moved.

We also said they pushed too far, and have been too slow to bring them back down. A lot of the inflation driving CPI was never going to be fixed by interest rates – it was outside of monetary policy’s reach.

For investors, that’s meant term investment rates sliding from 6% to under 4%. For borrowers, mortgage rates are now dipping under 5% (though half of borrowers haven’t felt the drop yet with fixed terms).

My personal opinion is that we’re going to see low interest rates for some time – good news if you’ve got debt, more of a squeeze if you’re relying on interest to supplement your income or saving.

Housing market: stability over sizzle

House prices have been making headlines too. Politicians are backing higher-density building in the most logical places for the bigger cities, and there’s even bipartisan chatter about keeping prices stable.

That’s good for productivity and for the next generation (including my kids, 19 and 25) if they decide to buy.

I might also add that I don’t agree with the current Government cutting the Kāinga Ora building programme – it was just really getting started.

Flat or gently falling prices mean more money flowing into productive investments, not just land speculation. And it highlights the real-world impact of your funds – through Squirrel, you’ve helped support thousands of new homes over the last five years, and with your backing we’re aiming to do much more in the next five.

Thinking of joining but haven't made the move yet? Join thousands of Kiwi already growing their money with Squirrel - Sign up in 5 minutes.

FundRock NZ Limited is the manager and issuer of the Squirrel Monthly Income Fund. The product disclosure statement can be found here.