- Get started on your mortgage

- Buying your first home, next home, investing in property or just keen to review your mortgage?

- Apply online

- Put your savings to work

- Earn better returns and access your money with no penalties.

- Start investing now

P2P Investor update – heading into week 2 of lockdown

It’s day 12 of the Covid-19 lockdown in New Zealand. The world is still feeling uncertain and whilst we don't have a crystal ball, what we can do is give complete transparency about how our P2P platform is doing. Firstly we’d like to reassure our investors that although nobody knew what was coming for us in 2020, our platform was carefully built upon the premise that things aren’t always rosy and our model allows for economic changes. You might actually be pleasantly surprised that it’s not all doom and gloom.

Here’s the latest on each of our investment classes, the behaviours we’re currently seeing, and most importantly how we’re managing it all.

Personal Loans portfolio update

As of close of business on Friday 3rd April, we’ve had 81 people enquire about loan payment deferrals or moving to interest only for a period. We expect we’ll see these requests continue to come in over the coming weeks.

In this instance, we work with each borrower to determine the best course of action for them. So far, 14 borrowers are deferring payments, and 4 have moved to interest only terms. This is planned for an average length of 2.6 months. The rest are still providing information. This support for our borrowers comes under the Credit Contracts and Consumer Finance Act (CCCFA) and is there to ensure lenders treat borrowers fairly, and support them when times are tough - which they undoubtedly are for a group of our borrowers who never expected to find themselves in this position.

Personal Loans arrears and the Reserve Fund

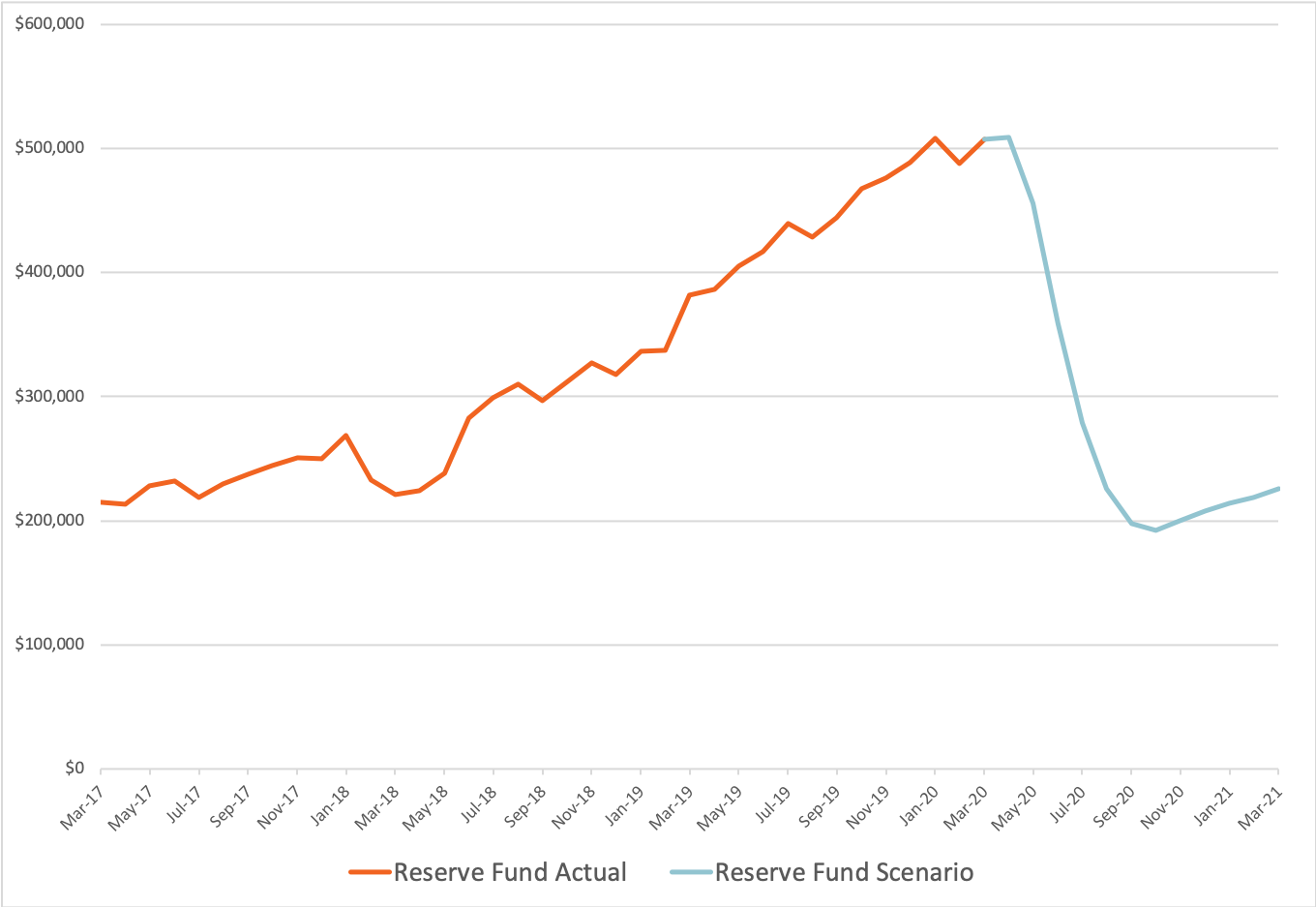

We’ve done some modelling work to understand what might happen if hardship increases and we see an increase in arrears. If we combine both categories, and assume an unemployment rate of 11% (we could expect unemployment to reach this level) for 3 months, with gradual improvement beyond that point, then this graph demonstrates what may happen. For perspective, each of the major NZ banks' economic teams are forecasting unemployment to double from about 4.5% earlier this year, peaking at circa 9% between June and September, with a gradual recovery beyond that point.

Remember this is a scenario and not a forecast. There are a lot of assumptions that go into making this scenario, and we’ve taken a pretty conservative stance in how it’s constructed.

Personal Loan Reserve Fund balance with 11% arrears and hardship

What this graph shows and what it means for you, is that the Reserve Fund would do its job and cushion the blow from borrowers who are unable to pay for a period of time.

All investors would continue to receive their fortnightly or monthly payments throughout this period IF the scenario we have put together is about right. In fact, even if the arrears rate (including hardship) gets to 15%, the Reserve Fund would still have the cover for investors to continue to receive repayments as normal. We will continue to refine the scenario as information starts to emerge on just how deep this recession will be, and how we see the portfolio performing.

Security over Personal Loans

If things turn really bad, then the most obvious question relates to the security we have in place with our borrowers. In our Personal Loan investment class today, it roughly breaks down into thirds:

- One third secured over residential property;

- One third secured over a vehicle or transportable tiny home; and

- One third unsecured

So about two thirds of our borrowers have offered up some form of security, and this is typically where the loan’s original value was over $20,000. We’ll be doing our best to help borrowers through these challenging times as humanely as possibly so that we do not have to call on that security.

Home Loans and Business Property Loans

As you are aware, these are new investment classes, opened in mid-March.

At present there are no concerns from our borrowers whose loans we have passed on to investors.

- It’s possible that we may need to extend the term of the loan for loans where construction is taking place as a result of the shutdown period when building work cannot happen.

- A Reserve Fund is set up for each of these investment classes. Squirrel has made $100,000 available for each of these Reserve Funds to kick start them. The first levys to each Reserve Fund will be paid in mid-April.

- All loans in each of these investment classes are secured over residential land/property with a first mortgage. There is strong security for these loans.

You can keep track of the Reserve Funds and portfolio statistics on our investor page.

What are other investors up to?

Two things stand out to us over the last month:

- We’ve seen a small number of investors transfer their Personal Loan investments via the secondary market, and from what they tell us, they’re moving their money back to cash in the bank. Some have also partially moved money back to cash to look for opportunities in other types of investments (like shares).

- This has also coincided with the biggest inflow of new money we’ve ever seen into our investing platform during February and again in March.

Since we launched the Home Loan and Business Property Loan investment classes mid-March, we’ve been watching investor behaviours and this is what we’re seeing:

- Some investors have taken a small bite ($500 or $1000), and appear to be watching what happens with these investments before committing more funds to them.

- Some investors have moved some large lumps of money (eg $50,000) from outside Squirrel, and invested into one or both of these new investment classes. At the moment we’d expect to see investors placing money with a higher weighting into the Home Loan and Business Property Loan investment classes relative to Personal Loans for the time being.

That's it for now

We’ll continue posting updates on how the portfolio is performing over the next wee while, and continue to give our investors as much information as is available. Strange times, but we’re in it together.

Enjoying our blog? Get the latest sent straight to your inbox

Receive updates on the housing market, interest rates and the economy. No spam, we promise.

The opinions expressed in this article should not be taken as financial advice, or a recommendation of any financial product. Squirrel shall not be liable or responsible for any information, omissions, or errors present. Any commentary provided are the personal views of the author and are not necessarily representative of the views and opinions of Squirrel. We recommend seeking professional investment and/or mortgage advice before taking any action.

To view our disclosure statements and other legal information, please visit our Legal Agreements page here.