- Get started on your mortgage

- Buying your first home, next home, investing in property or just keen to review your mortgage?

- Apply online

- Put your savings to work

- Earn better returns and access your money with no penalties.

- Start investing now

The bank profit bonanza during our cost-of-living crisis

Post by David Cunningham - Chief Squirrel

The banks are up to their old tricks this week, once again lifting mortgage interest rates.

This time, the move comes from ANZ, which has just announced it’s lifting its home loan interest rates across the board by between 0.10% and 0.26%.

The announcement comes hot on the heels of news, just last week, that inflationary pressures are easing — a clear sign that all the rate hikes we’ve had to date are working exactly as they need to.

It also comes at a time when the Reserve Bank has seen fit to hold off on any further Official Cash Rate (OCR) hikes for several months, and with New Zealand already in the thick of a cost-of-living crisis.

So, if all the evidence suggests no further hikes are needed, what justification has ANZ offered up for the move?

It said the changes reflect recent increases in wholesale swap rates — with its spokesperson going on to say:

“Interest rates will continue to be reviewed in response to international and local market conditions. When reviewing interest rates we consider a range of factors, including the impact on customers, the underlying cost of funds (including wholesale rate movements) and competitor activity.”

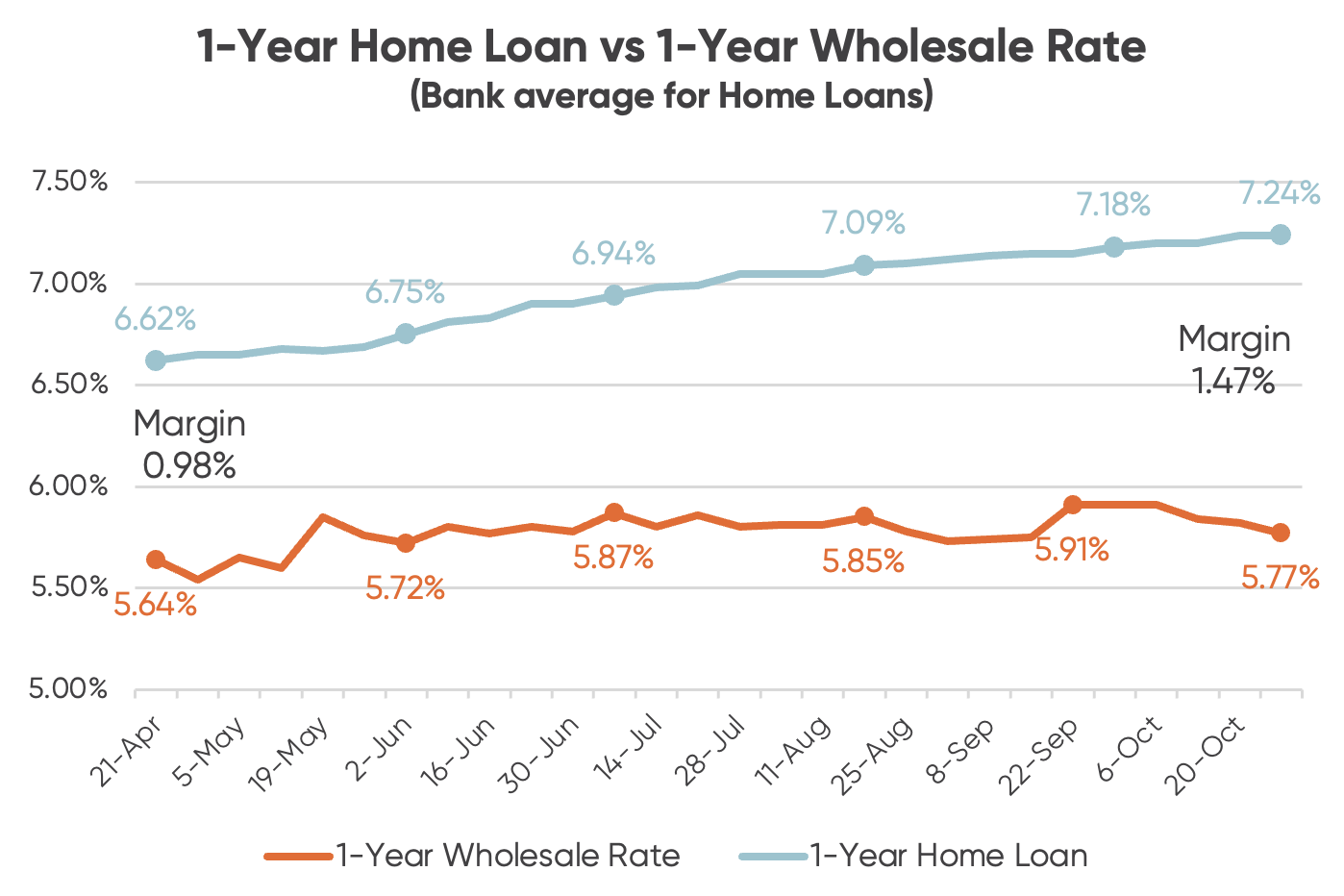

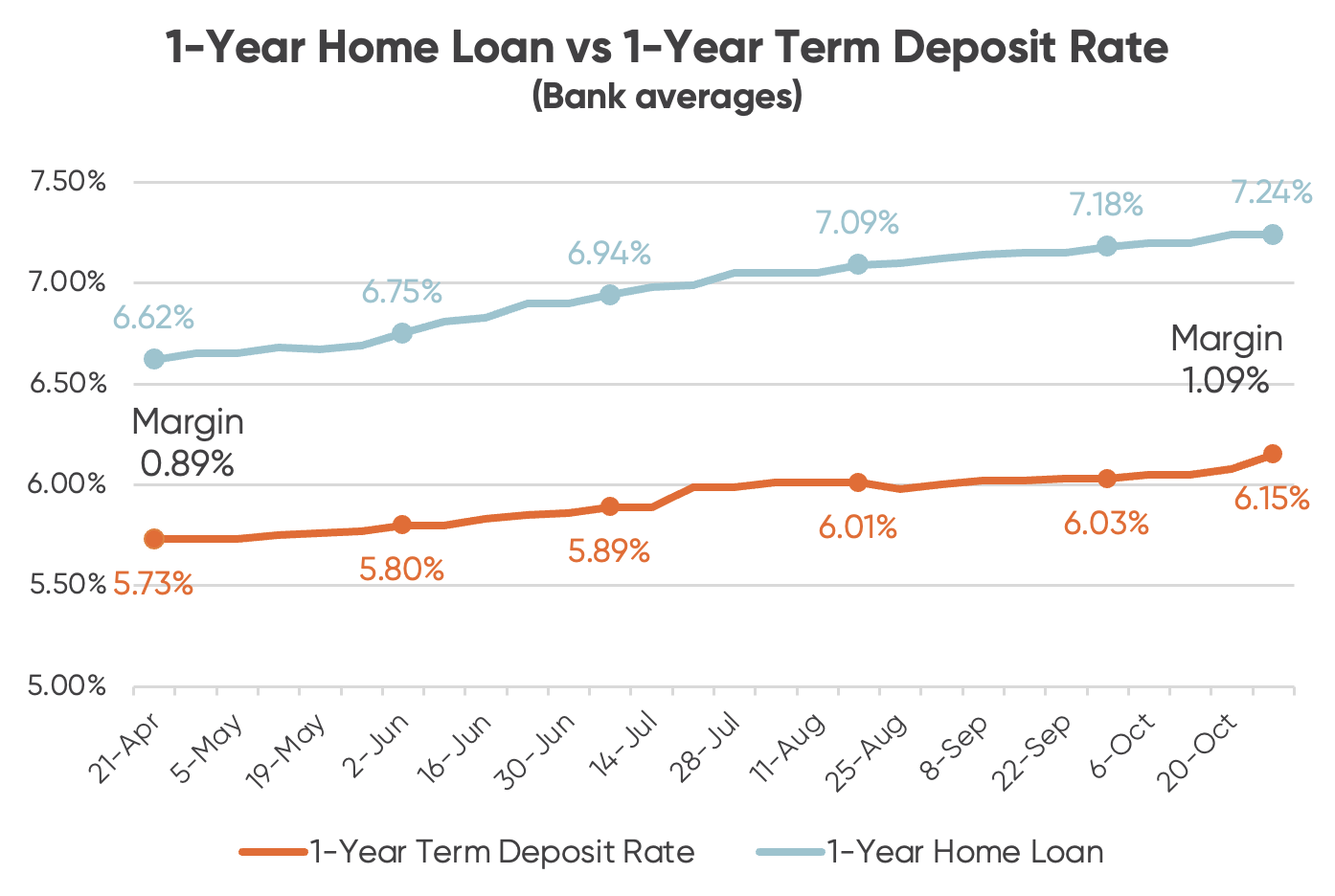

So, let’s test that justification then, using the popular one-year term as the example.

The charts below track the average bank home loan, term deposit and wholesale interest rates (which is the benchmark against which the banks set their interest rates for customers).

Data source: interest.co.nz

As you can see, the one-year wholesale interest rate has barely moved since 24th May, when we had our last OCR hike.

And yet, since then, banks have lifted their 1-year fixed home loan rates by about 0.5%. That’s equivalent to a double (or 0.50%) OCR hike!

It’s important to note that Term Deposit rates have also lifted over this post-OCR hike timeframe, but by less than the 1-year home loan rate (about 0.35%). And again, the margin is now much wider than it was previously.

For ANZ in particular, the reality is richer still, given their one-year home loan rate has just risen to 7.39%, while its one-year term deposit rate sits below the market average, at 6.1%.

While the rest of us suffer a cost-of-living crisis, ANZ (and the other banks) continue to celebrate a profitability bonanza.

Fair? You be the judge.

Enjoying our blog? Get the latest sent straight to your inbox

Receive updates on the housing market, interest rates and the economy. No spam, we promise.

The opinions expressed in this article should not be taken as financial advice, or a recommendation of any financial product. Squirrel shall not be liable or responsible for any information, omissions, or errors present. Any commentary provided are the personal views of the author and are not necessarily representative of the views and opinions of Squirrel. We recommend seeking professional investment and/or mortgage advice before taking any action.

To view our disclosure statements and other legal information, please visit our Legal Agreements page here.